Outlook for Business Loan Interest Rates in the United States (2026–Beyond)

The landscape for business loan interest rates in the United States remains a key factor influencing small and medium-sized enterprises’ (SMEs) financing decisions. As we move through 2026, several economic signals are shaping expectations around borrowing costs and lending activity.

Current Interest Rate Environment

As of early 2026, the U.S. Federal Reserve has kept its benchmark policy rate steady at 3.50%–3.75%, deciding against further cuts for now due to persistent inflation and a stabilizing labor market. Policymakers have emphasized that future decisions will be data-driven rather than pre-committed to cuts. (Reuters)

This stance keeps a floor under interest rates broadly, which in turn affects business loan pricing. For small business and commercial lending, bank and online lender rates can vary widely depending on creditworthiness, loan type, and term length. For example, according to recent industry data, interest rates on typical business loans can range from mid-single digits for strong bank borrowers up into the high teens or beyond for online or alternative lenders. (Bankrate)

Economic and Lending Trends Influencing Rates

Recent surveys from the Federal Reserve suggest that loan demand among U.S. banks is expected to strengthen in 2026, particularly for business loans across all categories, with demand highest among large and medium firms. Small business loan demand has remained relatively flat but stable, and lenders are not broadly tightening standards further. (Reuters)

This dynamic—steady interest rates alongside firm lending appetite—could support business borrowing activity even without significant rate cuts.

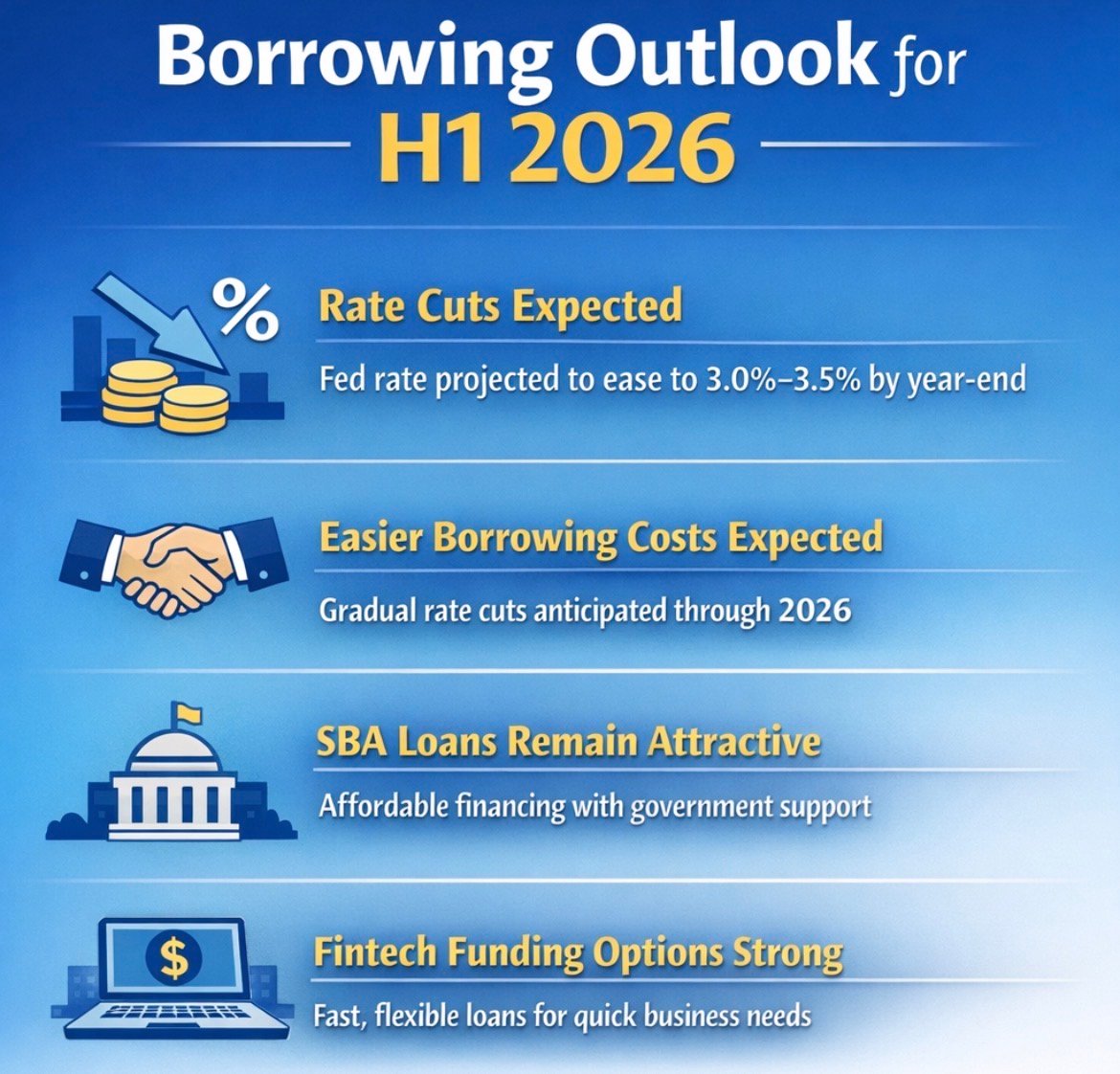

Rate Forecasts and Market Expectations

While the Fed has paused cuts, financial markets still price in the possibility of modest rate reductions later in the year, with some futures markets anticipating cuts potentially in mid to late 2026. These expectations are shaped by inflation trends and economic data. (Reuters)

However, some policymakers and analysts suggest that the current rate level may be near neutral—meaning neither stimulative nor restrictive—reducing urgency for near-term cuts unless inflation falls more decisively toward target levels. (Reuters)

What This Means for Business Borrowers

Because interest rates are influenced by broader monetary policy and economic conditions, business owners should monitor trends in Federal Reserve decisions, inflation reports, and credit market developments when planning financing strategies.

Current Business Loan Interest Rates in the U.S.

- Traditional bank business loans: 6.5% – 9.5% APR

- SBA loans (SBA 7(a), SBA 504): 7.0% – 10.5% APR

- Online / alternative business lenders: 10% – 25%+ APR