First Half of 2026: Smart Borrowing in a Changing Rate Environment (U.S. Outlook)

Access to capital is expected to remain generally available in the first half of 2026, even as interest rates evolve from their post-pandemic highs. While borrowing costs have been above the ultra-low levels seen earlier in the decade, forecasts suggest that monetary policy in 2026 will likely shift toward modest easing, creating potentially more favorable conditions for financing growth and investment.

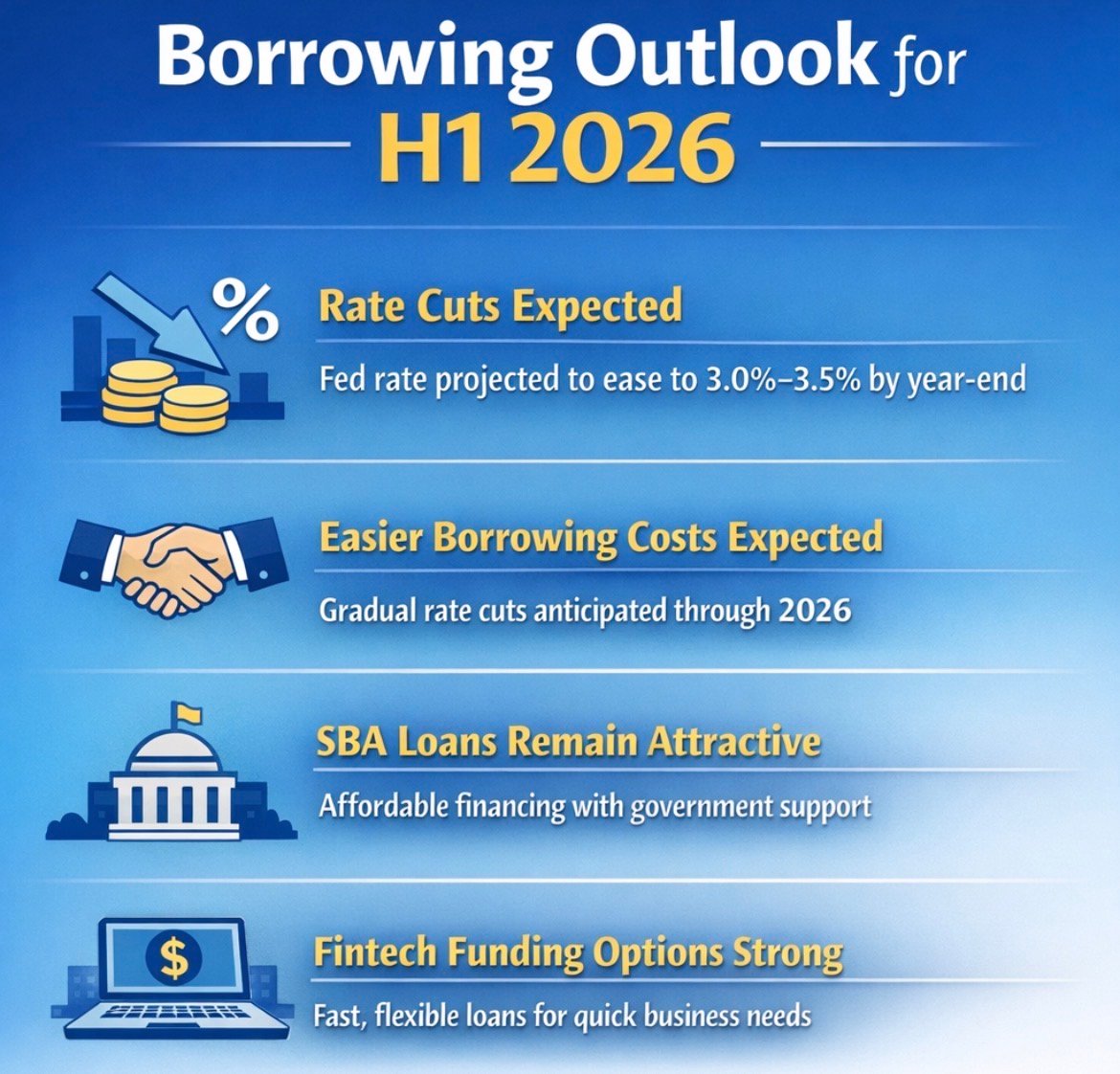

Interest Rates: Expectations for Gradual Declines

Rather than a permanently “higher-for-longer” environment, many analysts and economists now anticipate that the Federal Reserve will continue reducing the federal funds rate through 2026. Markets and institutional forecasters largely forecast one to a few rate cuts over the year, which could bring the federal funds target down to approximately 3.0%–3.5% by year-end.

• Research from major financial institutions like Goldman Sachs suggests the Fed may slow the pace of easing early in 2026 before delivering cuts in the spring and early summer, potentially bringing the policy rate into the mid-3% range.

• Market-based models also estimate 1–2 additional rate cuts during 2026, gradually lowering the terminal rate further.

This expected easing reflects steady progress on inflation and the Fed’s efforts to balance price stability with supporting economic growth.

SBA Loans Still Attractive as Cost of Capital Shifts

SBA 7(a) and other government-backed loans should remain an attractive option in 2026, particularly if central bank easing reduces borrowing costs. Even with future rate cuts, business loan APRs will likely stay above the ultra-low levels of the early 2020s, but employers may find improving affordability over time if policy rates decline as forecast. Preparation, strong cash flow, and clear investment plans will continue to boost approval chances.

Fintech and Alternative Lenders: A Competitive Edge Continues

Alternative lenders and fintech platforms are expected to sustain strong demand in 2026 because of their speed, flexibility, and tailored underwriting, even as interest rates moderate. For businesses with time-sensitive needs or less-traditional credit profiles, these lenders can offer a useful complement to bank-based financing—especially for short-term working capital and growth initiatives.

Higher APRs in this space (often above traditional bank pricing) will likely persist, but the widening gap between speed and traditional rate improvements means many firms will continue to weigh timing and agility against cost.

Overall Environment for Borrowers in H1 2026

• Rate projections lean toward easing rather than further tightening. Markets and economists expect the Fed to cut rates gradually in 2026, helping reduce borrowing costs over time.

• Access to capital should remain broadly available for creditworthy borrowers with strong financials and clear plans.

• SBA and alternative financing channels will remain relevant, with fintech lenders offering speed alongside banks’ more competitive pricing in a gradually easing environment.